Stock Market vs. Real Estate: Which is the Better Investment?

When it comes to building long-term wealth, few debates are more common—or more polarizing—than stocks vs. real estate.

On one side, you’ve got the stock market: fast-moving, accessible, and backed by over a century of data showing consistent growth. On the other, real estate: a tangible asset class that builds equity, generates monthly cash flow, and has helped millions create generational wealth.

Both have created millionaires. Both carry risks. And both require a strategy that matches your personal goals.

But which one is right for you?

That’s exactly what this guide will break down—with clarity, not hype. We’re going to compare these two powerhouse asset classes across five core factors:

- Historical performance

- Risk and volatility

- Liquidity and time commitment

- Entry costs and accessibility

- Tax treatment and control

By the end, you won’t just know which is “better.” You’ll know which is better for your specific situation, mindset, and long-term plan.

Let’s get into it.

How to Build a Diversified Investment Portfolio (2025)

Quick Definitions – What Are We Actually Comparing?

Before we start comparing returns, risk, and strategy, let’s define what we actually mean by “investing in the stock market” and “investing in real estate.” These aren’t just labels—they represent very different approaches to growing your wealth.

What Is Stock Market Investing?

Investing in the stock market means buying partial ownership in companies, usually through:

- Individual stocks (e.g., shares of Apple, Tesla, etc.)

- Index funds (e.g., S&P 500 funds that track the overall market)

- ETFs (Exchange-Traded Funds that hold a basket of assets)

- Dividend-paying stocks (which provide income in addition to growth)

- REITs (Real Estate Investment Trusts – more on that later)

Most stock investments are made through brokerage accounts or retirement accounts like IRAs or 401(k)s. They’re accessible, easy to manage, and historically strong over long periods.

What Is Real Estate Investing?

Real estate investing means buying property with the intent of generating income or appreciation. This can include:

- Residential rental properties (single-family homes, duplexes)

- Commercial properties (office buildings, retail space)

- Vacation rentals (Airbnb or short-term leases)

- Flipping real estate involves purchasing, remodeling, and then reselling for a profit.

- Land investing (undeveloped property for future value)

Real estate often involves a larger upfront cost, financing through a mortgage, and active involvement—especially if you’re managing tenants or doing renovations yourself.

Why This Matters

Too many people compare stocks and real estate as if they’re directly interchangeable. They’re not.

Stocks are liquid, abstract, and market-driven.

Real estate is physical, illiquid, and frequently location-specific.

Understanding what you’re really investing in helps you choose the right asset—not based on hype, but on how well it fits your risk tolerance, capital, and lifestyle.

Historical Returns: What the Data Really Says

When people ask “which investment is better,” they’re usually asking which one makes more money. So let’s look at the numbers.

Over the long term, both the stock market and real estate have delivered solid returns—but not in the same way, and not without trade-offs.

Stock Market: Consistent Growth Over Time

The benchmark index of the top 500 American corporations, the S&P 500, has historically produced returns of 7% to 10% per year after inflation.

- This includes both capital appreciation (stock prices going up) and dividends paid out to shareholders.

- Reinvesting dividends usually results in even greater returns for investors over time.

- Importantly, it’s passive—no tenants, no property management, no phone calls at midnight.

Dividend Stocks: A More Stable Subset

Dividend-paying stocks have slightly lower capital gains but provide regular income and often outperform during market downturns. When reinvested, they have historically yielded yields of about 7% annually.

Real Estate: Steady Returns, Boosted by Leverage

Real estate tends to appreciate at an average of 3% to 5% annually, but with rental income and tax advantages, total returns often hit 6% to 8%—especially when held long-term.

Here’s where it gets interesting: leverage.

- A 20% down payment lets you control 100% of a property.

- If property values increase, your return on the invested capital is magnified.

- This leverage is what allows many real estate investors to hit double-digit returns.

But leverage also amplifies losses, which makes real estate potentially riskier in downturns.

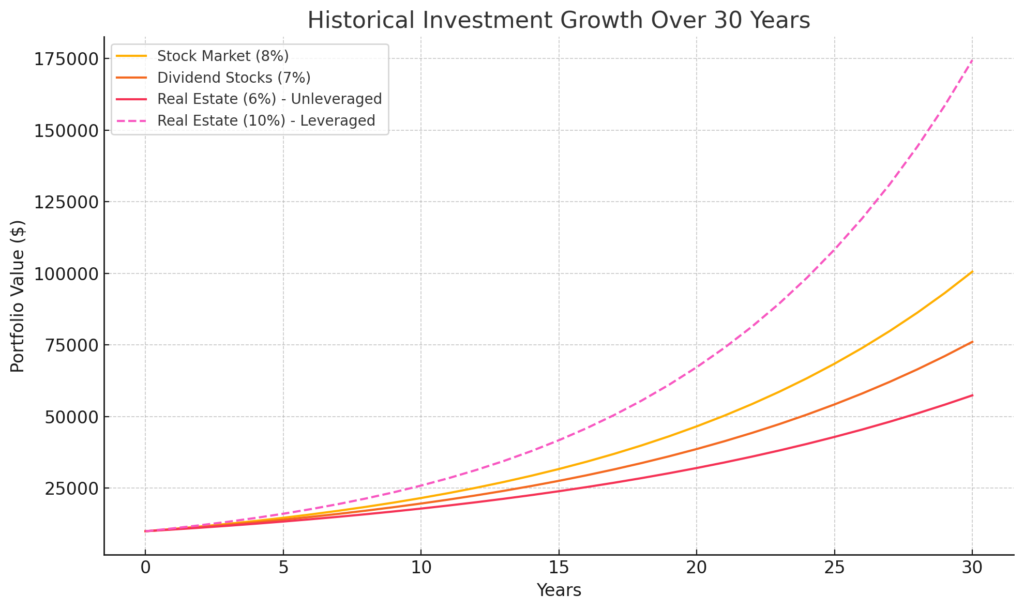

Visual Comparison: 30 Years of Growth

As the chart above shows:

- The stock market grows steadily with compounding returns.

- Dividend stocks lag slightly but provide income along the way.

- Real estate grows slower when unleveraged.

- Leveraged real estate (with mortgage financing) can outperform—but also carries more risk and responsibility.

Bottom line: Stocks generally outperform without much effort. Real estate can outperform—but it requires smart leverage, active management, and a higher tolerance for complexity.

Risk Profiles: Volatility vs. Stability

Risk is a part of any investment, but not all risks are the same. Stocks and real estate both come with their own brand of uncertainty, and just as important as the numbers is how you react when the market shifts.

This is where behavior and mindset become just as important as returns.

The Stock Market: Fast-Moving, Emotionally Demanding

The stock market is volatile by nature. Prices can swing wildly based on interest rate news, earnings reports, political events, or even tweets.

Financial Risk:

- Market corrections, or declines of ten percent or more, are frequent.

- Recessions can drag markets down 30%–50% before recovery

- Long-term returns are diminished by emotional investors’ propensity to purchase high and sell cheap.

Emotional Risk:

- You see your money fluctuate every day

- Panic selling is common during downturns

- It requires trust in the long-term trend to stay the course

The stock market rewards patience and consistency—but it tests both constantly.

Best Stock Market Apps for Beginners in 2025 (Reviewed + Ranked)

Real Estate: Slower, But Not Safer

Real estate feels more stable because prices don’t change on a screen every second. But that doesn’t mean it’s risk-free.

Financial Risk:

- Property values can fall in recessions or local downturns

- Vacancy periods cut into rental income

- Major repairs or damage can quickly eat into returns

- Leverage magnifies both upside and downside

Emotional Risk:

- You’re on the hook for everything: tenants, maintenance, repairs, property taxes

- Bad tenants or legal issues can turn cash flow into chaos

- It’s much harder to “sell quickly” if things go wrong

Owning real estate gives you control, but also responsibility—and that can be stressful for people who want hands-off investing.

The Psychology of Each Market

Here’s what most blogs won’t say: the best investment is the one you can emotionally commit to during bad times.

- If you panic during market dips, stocks may feel overwhelming.

- If you hate dealing with people or repairs, real estate may wear you out.

- If you’re likely to overreact to short-term changes, volatility will hurt your results—no matter the asset.

Bottom line: Risk isn’t just about what could go wrong financially.

It’s also about what you’re mentally built to handle when things aren’t going your way.

Liquidity & Time Commitment

One of the biggest differences between stocks and real estate isn’t about money — it’s about access and effort. Specifically:

- How easily can you access your cash if you need it?

- How much of your time and attention does the investment require?

Let’s compare.

Stocks: Instant Liquidity, Minimal Time Required

When you invest in the stock market—especially through modern platforms like Fidelity, Vanguard, or apps like Robinhood—you can buy or sell your investments within seconds.

Liquidity:

- Stocks are highly liquid

- You can exit your position the same day in most cases

- No paperwork, no phone calls, no negotiations

Time Involvement:

- Once your portfolio is set, it’s mostly hands-off

- Rebalancing or reviewing performance can be done a few times a year

- Even dividend investing can be automated through reinvestment plans (DRIPs)

Bottom line: Stocks are ideal for people who want scalable wealth-building without adding another job to their schedule.

Real Estate: Equity That Moves at a Crawl

Real estate ties up your capital in a physical asset. If you want to access that money, the process is slow, complex, and often expensive.

Liquidity:

- Weeks or months may pass before a property is sold.

- You’ll deal with inspections, negotiations, and legal paperwork

- Closing costs, commissions, and taxes can significantly reduce your net gain

- Cash-out refinancing or HELOCs are options—but they come with fees and debt

Time Involvement:

- Managing property means managing people and problems

- Tenant selection, rent collection, upkeep, and repairs are among the duties.

- Outsourcing to a property manager adds cost (typically 8–12% of rent), but removes daily tasks

Even for passive income seekers, real estate is not truly passive unless you outsource operations—and even then, you’re still the owner, legally and financially responsible.

What This Means for You

If you want quick access to your money, stocks win by a mile.

If you’re okay tying up cash for longer periods—and are willing to manage or outsource the operational load—real estate can deliver cash flow and tax benefits in return for that effort.

Bottom line:

- Stocks = speed, flexibility, and freedom

- Real estate = locked capital and active involvement (or extra costs to make it passive)

Tax Treatment & Legal Considerations

You don’t get to keep 100% of your returns.

So while gross performance matters, net return—after taxes—is what really builds wealth.

And here’s where stocks and real estate take very different paths.

How Stocks Are Taxed

Stock investments are relatively simple when it comes to taxation—but they’re not always investor-friendly.

Capital Gains:

- If you sell a stock at a profit, you pay capital gains tax.

- Short-term (held <1 year): Taxed as ordinary income (higher rate)

- Long-term (held >1 year): Taxed at 0%, 15%, or 20% depending on your income

Dividends:

- Dividends that qualify are subject to long-term capital gains taxes.

- Non-qualified dividends are taxed as ordinary income

The Hidden Cost:

- Every time you sell, you trigger a taxable event

- Frequent trading reduces your compounding power due to constant tax friction

Best-case strategy? Buy and hold long-term, reinvest dividends, and minimize taxable events

How Real Estate Is Taxed (and Protected)

Real estate is far more complex—but often far more tax-advantaged if you know how to use the system.

Depreciation:

- You can depreciate the value of your property over time—even if it’s going up in value

- Your taxable rental revenue is decreased as a result of these paper losses.

1031 Exchange:

- Sell one property and roll the gains into another without paying capital gains tax

- As long as you follow the rules, you can defer taxes indefinitely

Mortgage Interest Deduction:

- If you own an investment property, deduct the interest you paid on your mortgage.

- This lowers your taxable income, especially in the early years

Operational Write-Offs:

- Maintenance, property management, insurance, travel, legal fees—all can be deducted

- These reduce your tax burden while preserving cash flow

Property Taxes:

- These are an annual cost, but they’re also deductible for investment properties

Which One Offers Better Post-Tax Returns?

It depends on:

- Your tax bracket

- How active you are in real estate management

- How long you hold your investments

But here’s the general breakdown:

| Investment | Taxes Work Against You | Or With You? |

|---|---|---|

| Stocks | Mostly against you — capital gains and dividend taxes eat into profits | ❌ |

| Real Estate | Mostly with you — depreciation, deductions, and 1031s lower taxable income | ✅ |

With the right strategy, real estate investors can pay very little in taxes, even while generating strong income. Stock investors have fewer options, and often end up paying more unless they’re holding long-term or using retirement accounts.

- Stocks are simpler and more transparent, but less flexible when it comes to tax planning.

- Real estate is complex, but offers serious tax advantages that can significantly boost your net returns—if you’re willing to do the work (or hire someone who is).

Entry Costs, Access, and Barriers

Returns and risk are important — but they don’t matter if you can’t get in the game.

Let’s compare how accessible each investment really is, and what the true costs are to get started.

The Power of Compound Interest: How to Make Your Money Work While You Sleep

Stock Market: Low Barrier, High Accessibility

The stock market has never been easier to access. With modern brokerages and investing apps, you can start with almost nothing and scale as you go.

Cost to Enter:

- As little as $1–$100

- Most brokers now offer fractional shares, so you don’t need to buy a full share of Tesla or Amazon to get started

Where to Start:

- Apps: Robinhood, SoFi, Webull (great for beginners)

- Robo-Advisors: Betterment, Wealthfront, Ellevest (automated portfolio building)

- Traditional Brokers: Fidelity, Vanguard, Charles Schwab (good for long-term planning)

Time to Execute:

- Open an account in minutes

- Start investing the same day

- No paperwork, no physical meetings, no gatekeepers

Bottom line: If you’ve got a smartphone and a bank account, you can start investing in stocks today.

Real Estate: High Capital, Higher Friction

Real estate offers major upside — but you’ll need significantly more money, patience, and paperwork to get started.

Typical Costs:

- Down payment: Usually 20% of purchase price (though FHA and VA loans can be lower)

- Closing costs: 2–5% of the property value

- Maintenance reserves: Experts recommend 1–3% of property value per year

- Emergency buffer: For vacancies, repairs, or tenant issues

Additional Barriers:

- Credit score requirements

- Debt-to-income ratios

- Legal compliance (landlord-tenant laws, inspections, insurance)

You also need time — not just to buy, but to manage, maintain, and monitor your asset.

What About REITs? The Hybrid Option

Purchasing stock in a real estate company is similar to investing in a REIT (Real Estate Investment Trust). It gives you real estate exposure without owning property directly.

- Traded on the stock market like any other stock or ETF

- Minimum investment often $50–$100

- Pays dividends, benefits from property appreciation

- Requires no management, no tenants, no upkeep

Popular REIT platforms:

- Publicly traded: VNQ (Vanguard Real Estate ETF), O (Realty Income)

- Private REITs: Fundrise, Streitwise, DiversyFund

If you want real estate exposure without the real estate headaches, REITs are the lowest-barrier bridge between both worlds.

Bottom line:

- Stocks are the most beginner-friendly entry point into investing — fast, cheap, and accessible to almost anyone.

- Real estate requires higher capital and commitment but can reward active involvement and smart leverage.

- REITs let you blend both strategies without the operational complexity of owning physical property.

When the Stock Market Might Be Better

The stock market isn’t just a wealth-building tool—it’s also a great fit for certain types of investors. If any of the following describes you, the stock market may be your more natural starting point.

1. You’re Just Getting Started With Limited Capital

If you’re working with a few hundred (or even a few dozen) dollars, real estate is likely off the table. But the stock market? You can invest with less than the price of a nice dinner.

- Fractional shares make even the biggest companies accessible

- Low or no account minimums

- No need to save for years before making your first move

2. You Prefer a Passive Investment Experience

Not everyone wants to deal with tenants, contractors, or property taxes. Stocks allow you to build a diversified portfolio that works in the background.

- Index funds and ETFs require zero day-to-day involvement

- Robo-advisors handle portfolio management automatically

- Rebalancing, dividends, and tax-loss harvesting can all be automated

If your goal is hands-off growth, stocks are the cleaner path.

3. You Want Flexibility and Liquidity

Things change. Life throws curveballs. If you need to access your money quickly or pivot your strategy, stocks make that easy.

- Sell your position anytime—no waiting, no paperwork

- Easily shift funds between sectors, strategies, or platforms

- Great for people who want to stay agile or reallocate as goals evolve

4. You’re Focused on Long-Term, Compound Growth

Stocks, especially through low-cost index funds, are built for long-term wealth. They benefit from decades of compounding, market cycles, and reinvested dividends.

- Historical average annual returns: 7%–10%

- No management required to grow over time

- Ideal for retirement accounts, long-term savings, and FIRE strategies

5. You’re Emotionally Comfortable With Market Fluctuations

Stocks move fast, and sometimes that’s uncomfortable. But if you can stomach short-term volatility and stay focused on the bigger picture, the stock market rewards long-term thinking.

If you’re the kind of person who:

- Doesn’t panic when things dip

- Understands market cycles

- Able to “buy and hold” in the long run

…then you’re built for stock investing.

Bottom line:

If you want low barriers, low maintenance, high flexibility, and long-term upside without active management, the stock market is likely the better place to start—or stay.

When Real Estate Might Be Better

Real estate isn’t for everyone—but for the right type of investor, it offers advantages that the stock market can’t match.

If any of the following apply to you, real estate might be the better long-term play.

1. You Prefer Tangible, Physical Assets

Some investors are more comfortable owning something they can touch, visit, and improve.

- You can walk through a property, renovate it, and increase its value

- It’s not just paper on a screen—it’s land, buildings, and real-world utility

- In uncertain markets, physical assets feel more “real” to many people

2. You Want Cash Flow and Appreciation at the Same Time

Rental properties offer two key forms of return:

- Monthly income from tenants

- Long-term appreciation as property values rise

Unlike stocks, where you often choose between growth and dividends, real estate can give you both—if you manage it right.

3. You’re Comfortable Using Debt (and Managing It Well)

Real estate lets you use leverage—borrowing money to control a more valuable asset.

- A 20% down payment gets you 100% of the appreciation

- Rents help pay off the mortgage while the asset grows

- Smart leverage can dramatically increase your total return

If you’re financially disciplined and understand how to use debt strategically, this can be a massive advantage.

4. You Want More Control Over Your Investment

With stocks, you’re a passive shareholder. With real estate, you’re the CEO of that asset.

- You choose the property, the tenants, the maintenance plan

- You can refinance, flip, enhance value, or raise rent.

- You make the calls—and you reap the rewards (or take the hit)

If you’re proactive, analytical, and like having control, real estate puts you in the driver’s seat.

5. You’re Willing to Put in the Work (or Build a Team)

Real estate isn’t passive—at least not at the beginning.

- You’ll deal with tenants, repairs, insurance, and paperwork

- Or you’ll hire people to do it for you—and manage them

If you see that as a challenge, not a chore, real estate gives you a scalable asset you can grow over decades.

Bottom line:

If you want control, cash flow, long-term appreciation, and the ability to build equity through smart leverage, real estate might be your lane—especially if you’re willing to treat it like a business.

Common Myths and Misconceptions

When it comes to investing—especially in stocks and real estate—there’s no shortage of half-truths, outdated beliefs, and straight-up bad advice.

Let’s clear the air.

Myth 1: “Real Estate Is Always Safer Than Stocks”

Reality: Real estate feels safer because it doesn’t fluctuate daily on a screen. But that doesn’t make it risk-free.

- Property values can drop—especially in local markets

- Real estate is leveraged, which magnifies both gains and losses

- Liquidity issues, bad tenants, or local economic shifts can wreck your returns

Truth: Although real estate is susceptible to risk, it can also be stable. It’s just a different kind of risk.

Myth 2: “Stocks Are Only for Wall Street Pros”

Reality: With today’s tools and access, anyone can start investing in the stock market with minimal capital and zero finance background.

- Index funds and robo-advisors make it easy to invest wisely without picking individual stocks

- Education and platforms are more accessible than ever

- You don’t need to “beat the market” to benefit from it

Truth: Stock investing is easier and more accessible now than it’s ever been—especially for beginners.

Myth 3: “You Need a Lot of Money to Invest in Real Estate”

Reality: Yes, real estate typically requires more capital upfront—but there are creative ways in.

- House hacking (renting out part of your home)

- FHA loans with a 3.5% down payment as low as

- Partnering with others to split costs

- Real estate crowdfunding platforms or REITs

Truth: Real estate is capital-intensive—but not impossible for beginners willing to get creative.

The fourth myth is that stocks are too erratic to be trusted.

Reality: The market goes up and down. It’s the price of admission for long-term growth, not instability.

- Historical returns still show strong upward momentum over time

- Volatility hurts only if you sell emotionally during downturns

- The longer your time horizon, the more volatility smooths out

Truth: Volatility is noise. Patience is the strategy.

Myth 5: “You Have to Pick One or the Other”

Reality: You can (and probably should) invest in both.

- Stocks provide liquidity, growth, and diversification

- Real estate adds cash flow, leverage, and tax benefits

- Together, they can balance out each other’s weaknesses

Truth: This isn’t a rivalry—it’s a portfolio strategy.

Don’t let old-school thinking or misinformation stop you from investing. Once you understand how each asset class really works, the myths start to fall apart—and the opportunities become a lot more clear.

The Hybrid Approach: Diversify for Strength

Stocks or real estate?

It doesn’t have to be a choice.

In fact, some of the most successful investors don’t pick one—they build wealth using both.

By combining stocks and real estate, you can create a portfolio that’s:

- More stable across market cycles

- More tax-efficient

- More tailored to your financial goals, timeline, and risk tolerance

Why Both Makes Sense

Each asset class has distinct strengths:

| Asset | Strengths |

|---|---|

| Stocks | Liquidity, passive growth, low barrier to entry, diversification |

| Real Estate | Tangible control, cash flow, leverage, tax advantages |

A hybrid approach allows you to:

- Use stocks for long-term compound growth and liquidity

- Use real estate for consistent income and accelerated returns through leverage

- Hedge one asset class with the other (e.g., stocks dip, real estate holds steady)

How to Start Investing with $100: A Beginner’s Guide to Building Wealth from Day One

Example: Balanced Portfolio by Risk Profile

Conservative Investor

- 70% Stocks (mostly dividend-paying and index funds)

- 30% Real Estate (REITs or a single rental property)

- Goal: Steady income + low volatility

Moderate Investor

- 50% Stocks (mix of growth and dividend stocks)

- 50% Real Estate (one or more rental properties or a mix of REITs and physical assets)

- Goal: Blend of growth, cash flow, and tax optimization

Aggressive Investor

- 30% Stocks (higher-risk growth stocks, sector ETFs)

- 70% Real Estate (leveraged residential or commercial properties)

- Goal: Maximize returns with hands-on involvement

This isn’t financial advice—it’s a strategic mindset shift:

You’re not betting on one asset class winning.

You’re building a system where multiple assets generate returns in different ways.

How to Start Blending Both

- Start with Stocks if Capital is Tight

- Build momentum with index funds and ETFs

- Use dividend income to pad savings or reinvest

- Use Stock Market Gains to Fund Real Estate

- Grow your down payment over time through your stock portfolio

- Move profits into rental property, a house hack, or REITs

- Reinvest in stocks using the cash flow from real estate.

- Take monthly rent income and automate investing into your brokerage account

- This accelerates compounding across both asset classes

The smartest strategy isn’t choosing between stocks and real estate.

It’s learning how to use both in sync—so you’re never relying on just one source of wealth, income, or growth.

Case Study: Two Investors, Two Paths, One Goal

Let’s look at how two hypothetical investors—one focused on stocks, the other on real estate—build wealth over 20 years. They start with the same income, same savings rate, and same long-term goal: financial independence.

Investor A – Stock Market Strategy

- Starts with: $20,000

- Contributes: $500/month into an index fund

- Strategy: Long-term, passive investing in low-cost ETFs

- Average annual return: 8%

- Reinvests all dividends

20-Year Outcome:

- Total contributions: $140,000

- Final portfolio value: ~$280,000

- No tenants, no repairs, no calls at 2am

- Portfolio is liquid and rebalanced annually

Investor B – Real Estate Strategy

- Starts with: $20,000

- Buys: $100,000 rental property with 20% down

- Rent covers mortgage + $200/month net cash flow

- Appreciation: 3% annually

- Rents increase 2% annually

- Reinvests cash flow into maintenance + savings

20-Year Outcome:

- Property value: ~$180,000

- Mortgage paid down: ~$70,000 equity

- Net monthly cash flow: ~$450/month (after adjustments)

- Total equity + cash flow value: ~$250,000+

- Ongoing involvement: property management, occasional repairs

What’s the Takeaway?

| Comparison | Investor A (Stocks) | Investor B (Real Estate) |

|---|---|---|

| Liquidity | High | Low |

| Time Involvement | Low | Moderate to High |

| Passive Income | None (until withdrawal) | Monthly cash flow |

| Maintenance Effort | None | Active (unless outsourced) |

| Return Potential | Strong w/ compounding | Strong w/ leverage |

Both investors built wealth.

Both strategies worked.

The difference came down to personal preference, discipline, and how hands-on each person wanted to be.

This isn’t about one “winning.” It’s about knowing which one fits you—or how to smartly use both.

Conclusion – Final Thoughts on Real Estate vs. Stocks

There’s no one-size-fits-all answer to the question:

“Which is the better investment—stocks or real estate?”

The truth is, both have the power to build serious wealth.

Both come with unique benefits, and both carry very real risks.

- The stock market offers unmatched liquidity, scalability, and simplicity for long-term growth. It’s ideal for hands-off investors who want to let compound interest do the heavy lifting.

- Real estate offers control, cash flow, and leverage—but requires more upfront capital, effort, and operational responsibility.

Neither is inherently better. The right choice depends on your capital, your goals, your timeline, and your risk tolerance.

Want cash flow and control? Real estate might be the move.

Want long-term growth with minimal time commitment? The stock market has your back.

Want true diversification and long-term financial resilience? Use both strategically.

Here’s the takeaway:

It’s not about choosing the perfect investment.

It’s about building a portfolio that works for you.

If you understand what each asset class brings to the table—and how to use them together—you won’t just be investing. You’ll be building real, lasting wealth.

SEO Disruptor | Paid Ads Architect | Content Alchemist | I don’t just rank pages

I build profit machines. From SEO domination to ads that print revenue, I turn digital noise into real-world business growth. Let’s connect